I started this blog to talk generally about markets and financial risk postures for them. But my discussions quickly diverted from things like M&A deal flow, debt issuance, and fed actions, their effects on sectors, etc., and maybe some technical issues such as models over to the macro-political after the fed extended its repo bailout to non-US banks, notably Deutsche. Since then, politicians, multinational organizations, and government bureaucracies have seized power, killed economic activity, and engaged in other historically egregious actions. Their effect on the overall picture has been so overbearing that discussing things like the relative advantages of some factor model approach relative to another for portfolio construction now seemed overly myopic ; like fussing to assemble a table setting, complete with a nice flower arrangement, on the deck of a ship that is likely to keel-over in the water. Rather than such portfolio risk foci, anyone providing risk management services to private high net worth clients should now be more focussed on giving them top advice on the best foreign countries in which to open bank accounts, obtain residency or a passport, perhaps buy an apartment, as well as move their businesses to (while they still can). But now that the biggest bulwark against the Great Reset, the USA, appears about to go-along with it, it remains to be seen if those jump-off countries will retain the economic freedoms that make them attractive now.

Before the MSM and big tech went ballistic with agitprop and censorship, before ANTIFA and BLM were allowed to conduct the most destructive civic insurrection in American history, before the WHO, IMF, UN, and WEF with Gates’ and Soros’ foundations and the heads of many nations started removing the freedom, rights, and livelihoods of their citizens and working on digital monies, I had written that the world economy was about to witness not just another single sovereign debt crisis, but the biggest multiple one ever. Sovereign insolvency in places like Greece, Zimbabwe and Weimar Germany resulted in crises in banking, their currencies, their economies, along with significant civil disruption and war. Today, we have most of the nations in the northern hemisphere as well as some below the equator simultaneously facing un-repayable debts. Half of the pension programs in Europe are already insolvent.

Unfortunately, it appears their response will be not to restructure the existing debt (e.g. into perpetual bonds), admit that they failed to manage all the socialist programs (retirement funds, pensions, medical benefits, etc.) that they promised to provide voters, step down, and skulk-away cowed. No, rather they seem to be banding together to do away altogether with what remains of real capitalism, which many of them say has failed (and has caused a climate crisis as well as systemic racism). And they are doing-so without any voting or other recourse to their citizens. They are aiming for some new form of global communist governance where they will remain ‘the elite’ in-charge, and all debt and private property will be ‘released’. That is an effective declaration of war against citizens who cherish their freedom and rights, their own country, and a continued voting voice in how it operates. The elites call this their war on ‘populism’ (ordinary people), which is more marketable than calling it a war on free democratic self-determination, yet it is still quite accurate.

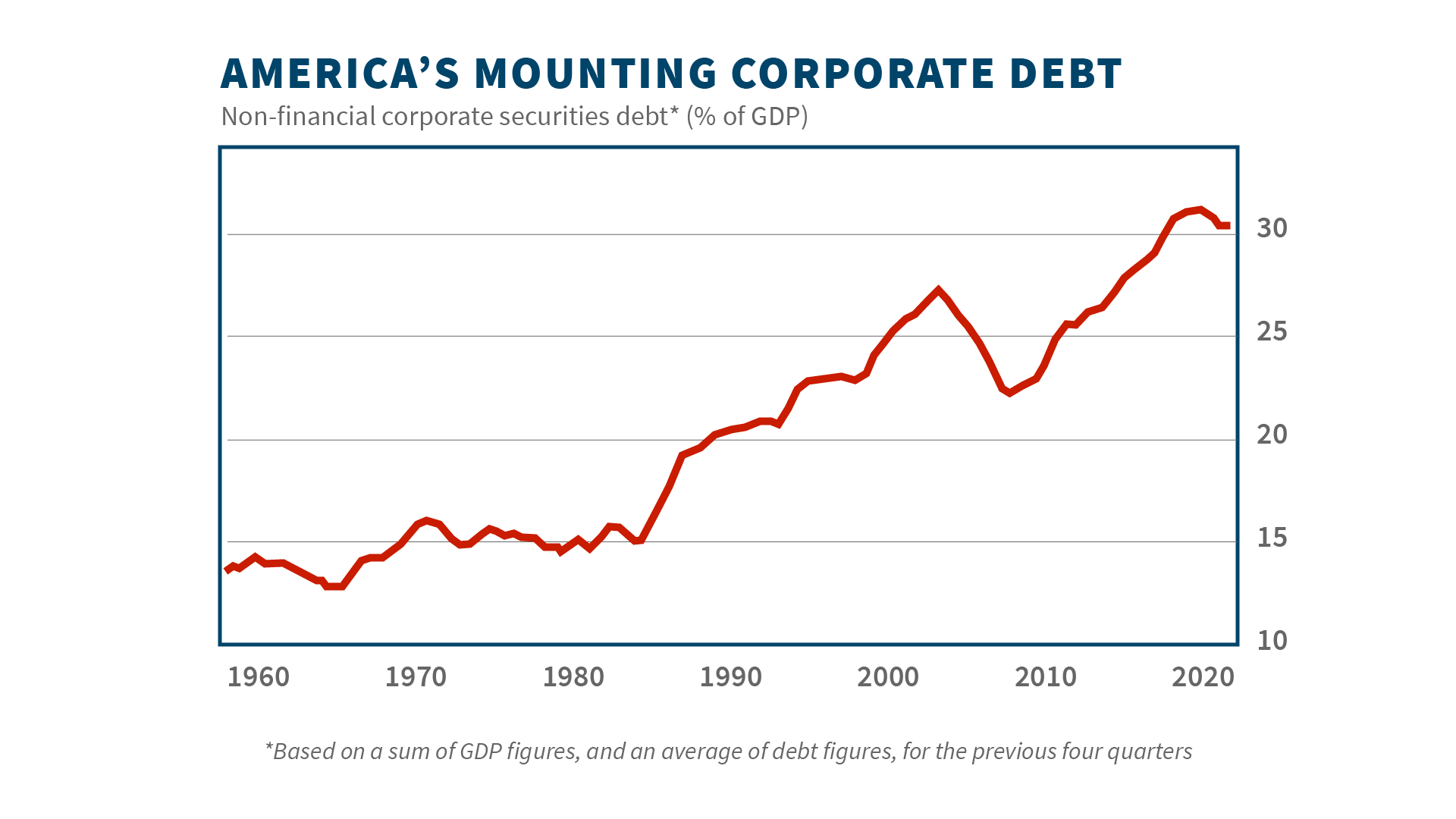

As abhorrent as all the Great Reset stuff is, it is clarifying to put it aside to review the expansion in debt and where we are in purely economic terms. Wall Street banks are obviously key players in the debt-growth story. A quid pro quo arrangement has existed for some time between the federal reserve and some of the biggest commercial banks in the country designated as ‘primary dealers’. These banks are authorized by the fed to deal directly with it, and act as its distribution channels for newly-issued treasury debt into the primary market. As such, they play a key role for the fed in implementing its monetary policy. In return, when those banks got themselves into fundamental liquidity problems, they were always given federal bailouts – Not just to stymie the extent of the illiquidity event, but also because if they failed, the fed could no longer respond by utilizing them to control the money supply. In 2008 following the collapse of Bear-Stearns, the fed backstopped the rest of them by setting up the Primary Dealer Credit Facility (PDCF) which enabled them to borrow overnight at its discount window.

During that crisis, the fed cut rates to zero, purchased $4.5 Trillion in Treasury and mortgage debt. It also directed $8 Trillion to bail-out banks and to extend loans to corporations. The purpose was to enable the banks to lend to businesses and consumers in order to stimulate the economy. But these banks and corporations kept most of it for themselves, and used it to take on new debt. Today in 2020, corporate debt issuance has exceeded a whopping $2 Trillion, fueled largely by the combination of nil rates and the solvency pressures imposed upon companies by the business lockdowns. The banks in 2008 did not inject the preponderance of the money into the economy as small business loans, and corporations did not direct it primarily towards the research and development and capital investment that would have led to the economic growth intended. They used it for non-productive purposes like stock buybacks.

Wealthy speculators borrowed the ‘free money’ to leverage up their financial assets; primarily stocks and real estate leading to run-ups of 160% and 60% in these respective markets from 2009-2015. While the wealthy did nicely, economic and wage growth were moribund, while housing, education, and medical costs rose substantially for the working class. Like the corporations, they filled their newly-expanded income-expenses gap with the cheap credit the fed had created. From 2006 to 2019, non-housing consumer debt soared from $2.2 to $4.2 trillion. Millennials racked-up $1.6 trillion in student debt (the only US debt configured to never be restructured nor forgiven), then found their degrees often worth little in the marketplace. Many seniors who worked hard over their lifetimes had their golden years taken from them as zero-rates flatlined the consistent retirement income they had setup with savings accounts, CDs, and other fixed income devices: Back to working a menial job at WalMart to pay the bills. The indebted social spending programs of municipalities and state governments also increasingly ran out of fiscal road.

The fed’s post-crisis actions effectively annulled the American social agreement (‘dream’) whose rules the educated had played-by; leaving many of them in serious financial straights. The class division has divertingly been painted opportunistically by elites as a racial/identity clash, as well as a systemic failure of capitalism. And of course, the solutions to both problems is again to keep themselves in power to continue to call the shots – only this time since the programs and bureaucracies they have run are bankrupt, they have to do that under the auspice of communism, an idea they have many young people believing ardently in due to their disillusioning experience combined with their postmodern educations.

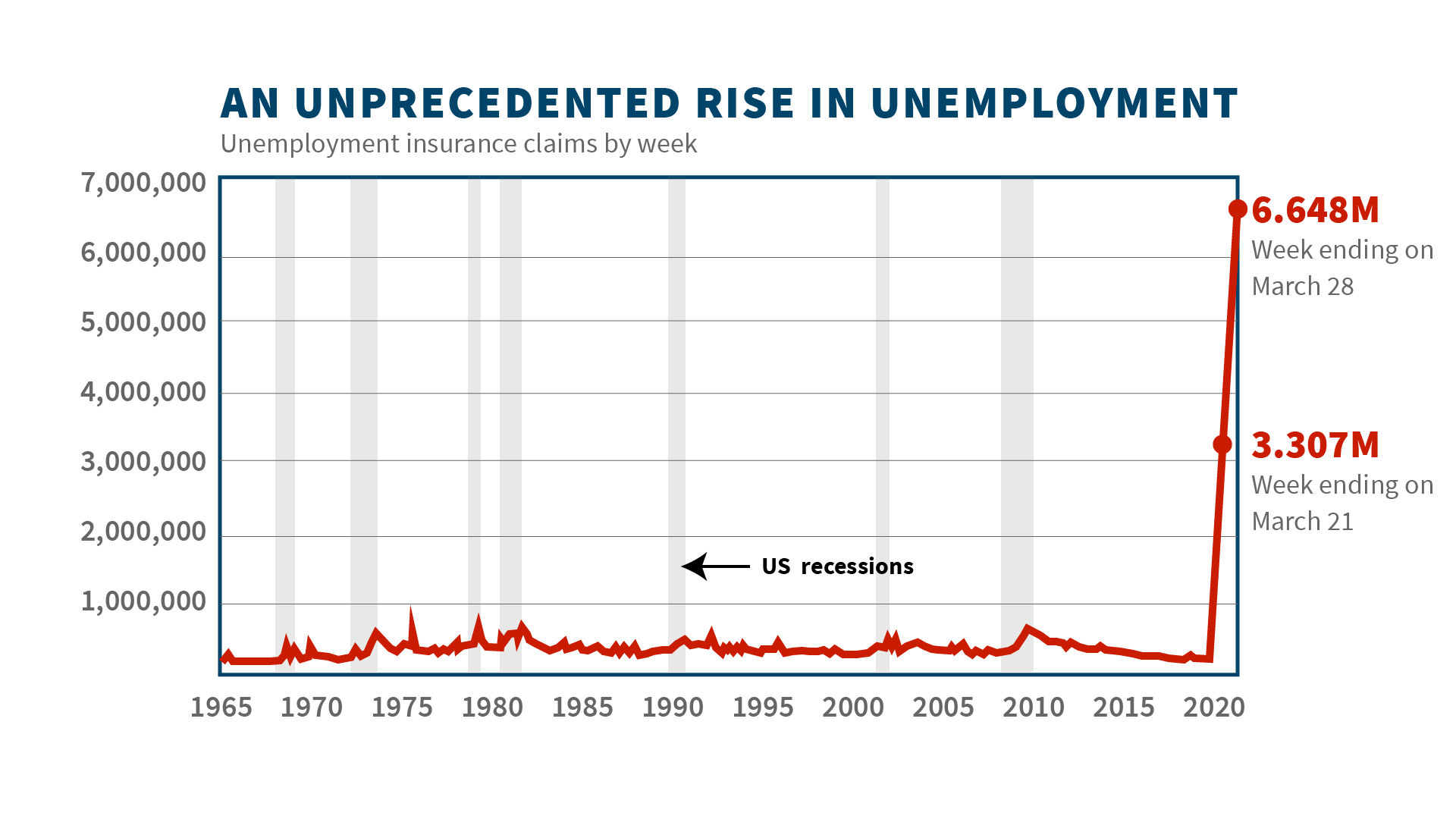

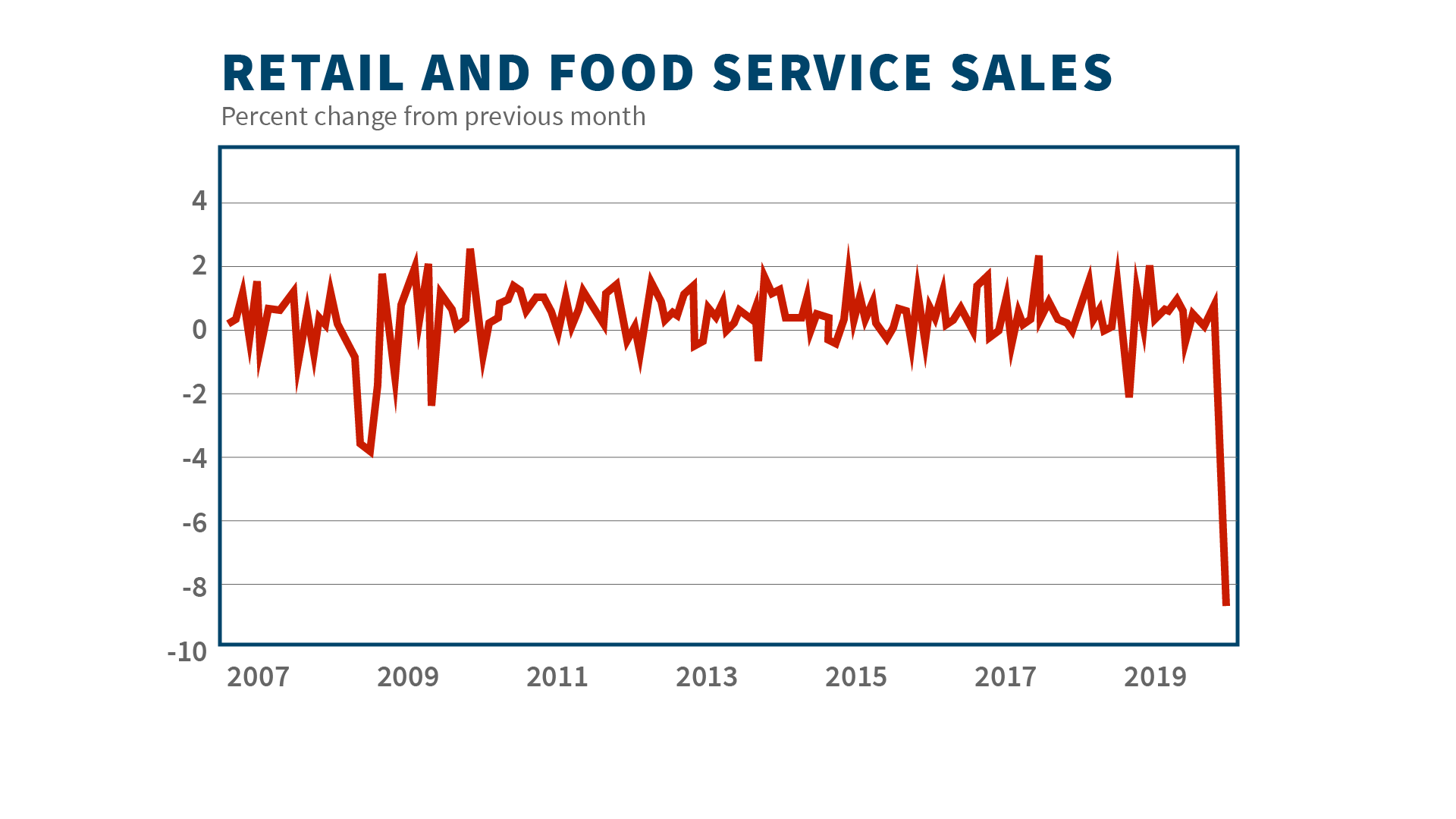

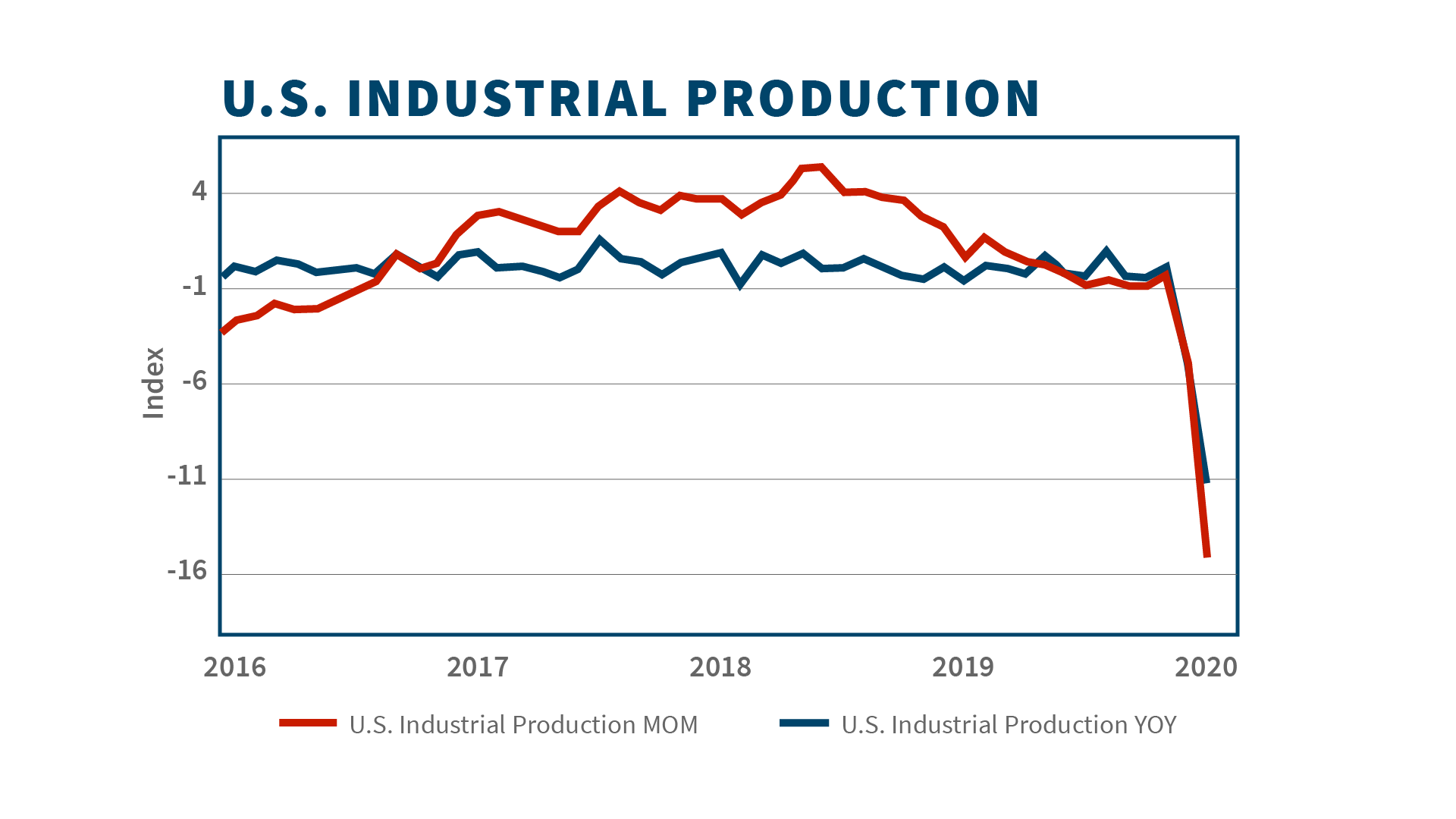

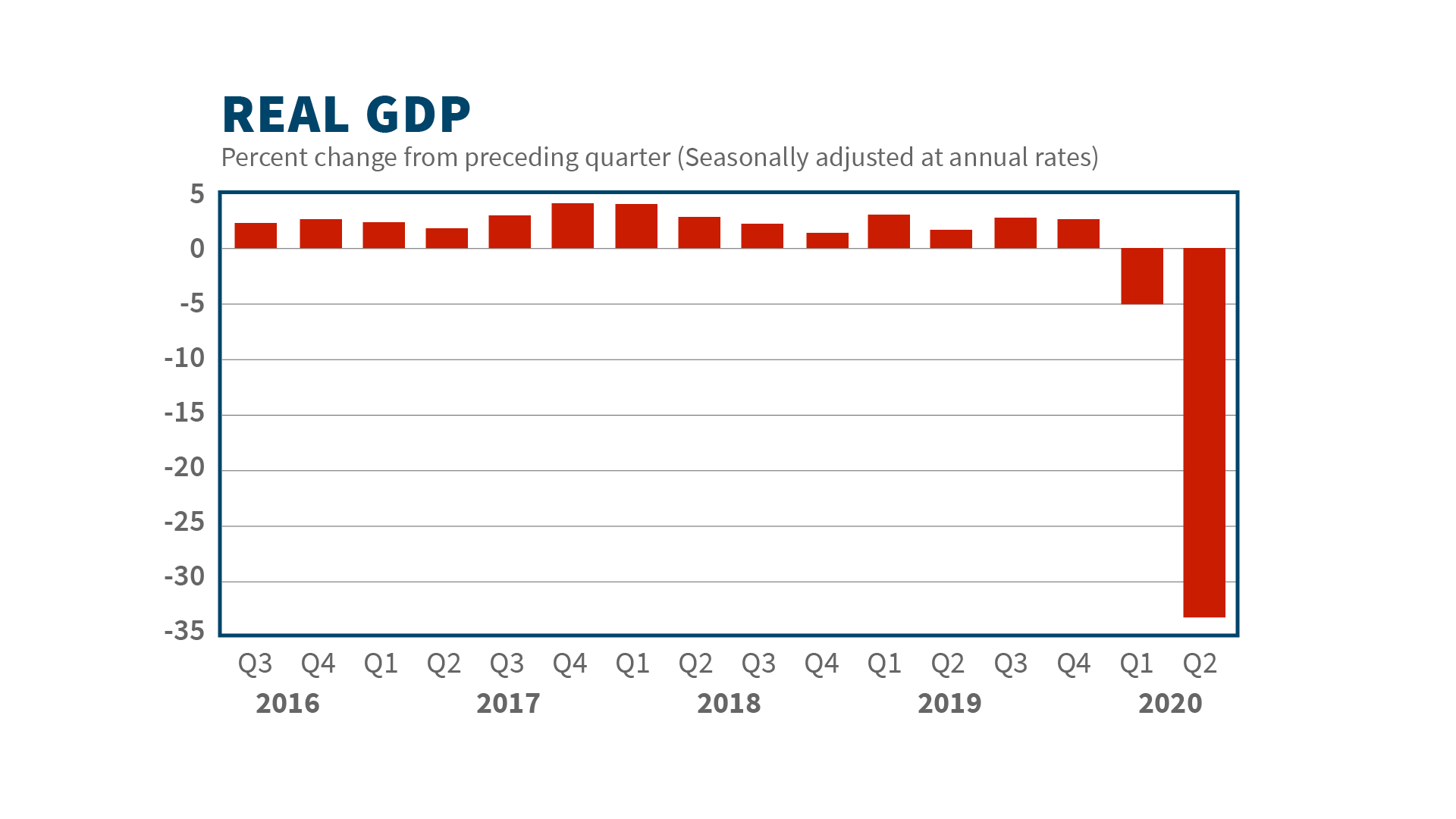

After a decade of QE and zero rates has failed to stimulate the economy (except for the window of time since Trump acted to lower taxes and thin the regulatory thicket until states locked down), the federal debt bubble had stretched to over $100 trillion (over $500 trillion if debt derivatives are included); over 3 times larger than 2008. Every player in the economy from the individual consumer to corporations to local and federal governments was historically levered-up. This mother of all US debt bubbles got the catalyst it needed to pop in in the form of the global Coronavirus shutdown – the first time in history that society decided that suspending its economy along with individual freedoms was the proper response to a plague. The stock market fell 34% in under a month, businesses closed, and Americans were thrown out of work. Many of these jobs are gone forever. The economic numbers shot-off to new levels far off their historic norms that required the vertical scales on all these plots to be expanded:

The final chapter in this somber saga: The fed and the government jumped-in again to keep a depression from striking. They spent over $6 trillion in just over a month by executing the following measures: Cutting interest rates from 1.25% to 0%. Buying commercial paper. Buying muni bonds, corporate debt, student debt, and even auto loans. Expanding the repo facility to $1 trillion per day. Launching a new $1.5 trillion repo program. Opening the discount window to the 8 largest US banks. Initiating a $700 billion QE program. And congress passed a $2 trillion rescue package and offered $350 billion in emergency loans to small businesses. To say they were improvising with their hair on fire is putting mildly.

All this has left our debt situation even in more ridiculous shape, and has delayed but has not circumvented this crisis. We have an economic crisis, not a monetary one, so money printing wont solve it. And with over 50 million thrown into unemployment, and more to come with the new federal lockdown on the way, consumer demand will just not be there – and consumer spending accounts for 70% of our GDP. The fed is expecting a 25% unemployment rate, on-par with the great depression. Mortgage delinquencies are already up over 20%, chapter 11 filings are up over 50%. Furthermore, the supply chains of many goods have been disrupted, including those for food. Cocoa, corn, and other crops are in backwardation. There’s a possibility we may have to play hunger games.

When the relief programs end, corporations will burn through their cash, the bankruptcy filings will soar, and liquidity will dry up. Mortgages and other loans will default, and the amount of debt banks will have to write-off will spike. Many banks have already given their borrowers forbearance on their debt payments for months, but they cant continue without that income for too much longer. On January 15, Chase, Citi, and Wells Fargo all will report their earnings. That glimpse into their balance sheets is likely to startle and could kill confidence to the point of restarting the collapse. We may see markets, banks, and tax revenues sharply down, joblessness, poverty, and the national deficit sharply up. And more debt creation will not stimulate as long as demand, supply, solvency, and confidence are absent. Social unrest will no longer be confined to groups like ANTIFA and BLM. Even more draconian crackdowns on liberty and property will be imposed.

I tried to run through all that economic loveliness without bringing-in the recent authoritarian stuff (although obviously things like the overbearing international COVID lockdown had to be mentioned). The point I wanted to illustrate is that even without a bunch of globalist oligarchs pursuing schemes out of a James Bond novel, we were in for historical trouble that will reshape the economic landscape (again). No matter who holds political office now, we have two things that are fundamentally destabilizing: (i) A very serious sovereign debt crisis that is the biggest by-far, and (ii) A much more stratified society in which the majority is more poor and disenfranchised, and the where the elite minority is more powerful and wealthy than ever. Having suggested that the debt bubble’s eventual pop may now be impending, a crisis that elites would not let go to waste, let me revert back to the Great Reset scheme to note a potential opportunity that fresh banking crisis may present for it:

There is scuttlebutt that the Great Resetters in governments intend not to bail out the commercial banks in any upcoming crisis. The speculation is that the imposition of centralized federal electronic monies and digital monitoring will be facilitated by their ideological allies in big tech who sit at the-ready with their Google Wallets and Apple Pays ready for conversion and integration into any upcoming CBDC. Even if they receive only the tiniest of transaction fees for this servicing, it will increase their power enormously since that fee will apply to every transaction in the economy.

If commercial banks are allowed to fail and are to be replaced by big tech finance operators, FinTech will at-once become a much more encompassing ‘sector’. There are many regulatory requirements to work though for tech companies to become able to conduct banking operations, but they hold only as long as the present system of rules pertains. I have no idea if a Machiavellian economic restructuring would actually go this far, and I expect they will fail to if they try one. Even if Biden’s administration is willing to go along completely with Klaus Schwab’s vision, it seems impossible to implement it with the current lineup in congress. But in this current debt-comeuppance phase of western civilization, the wild and unexpected is no longer flatly dismissible: Apparently John Kerry is going to become the US government’s first ‘Climate Czar’, and there is buzz that AOC may be appointed as administrator of the Environmental Protection Agency. What a relief !

The commercial banks have received liquidity-backstopping from the government (the fed) because they obviously have provided crucial functions for our market system, including corporate debt & equity issuance, IPOs, M&A deal-making, securitizations, market-making, etc. It seems crazy to just discard all that expertise, unless the next generation of communism is about to be ushered-in. The system that is in-operation in China is not communism in its purest sense, because people are still allowed to own things there and to run their companies. But in a pure communist system, investment and commercial banking is a much simpler operation run, like everything else, by the central state who is the lone voice in how things operate. The banks have worked very closely with the federal reserve and they still have influence. It might be worth exerting it now.